When you’re juggling multiple credit card bills, personal loans, and other debts, every month feels like a financial tightrope walk. You’re not alone. Many Singaporeans face this exact situation, and the stress can feel overwhelming. The good news? You have options. Two popular strategies stand out: debt consolidation and debt management. But which one fits your situation?

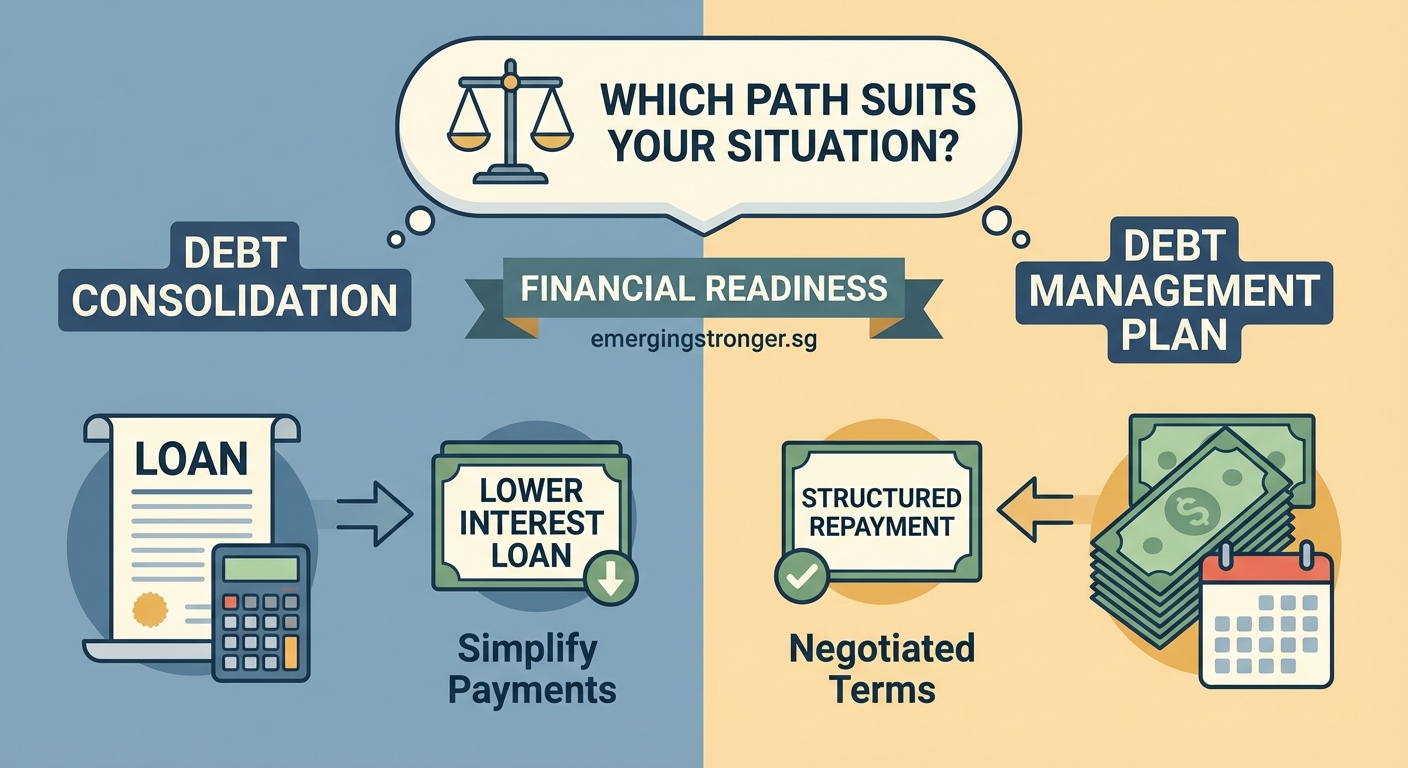

[Debt consolidation](https://en.wikipedia.org/wiki/Debt_consolidation) combines multiple debts into one loan with potentially lower interest rates, ideal if you have good credit. Debt management plans work through credit counselling agencies to negotiate reduced payments and rates, better suited for those struggling to meet minimum payments. Your credit score, monthly budget, and financial discipline determine which path helps you regain control faster.

Understanding debt consolidation

Debt consolidation means taking out a single loan to pay off multiple existing debts. Think of it as bundling everything together under one roof.

You apply for a personal loan or balance transfer facility. If approved, you use that money to clear all your other debts. Now you have just one monthly payment instead of five or six.

The main appeal? Lower interest rates and simplified payments.

Most credit cards in Singapore charge between 24% to 28% per year. A consolidation loan might offer rates between 6% to 12%, depending on your credit profile. That difference can save you thousands of dollars over time.

Here’s how the process typically works:

- Review all your current debts and their interest rates

- Check your credit score with the Credit Bureau Singapore

- Compare consolidation loan offers from banks and licensed moneylenders

- Apply for the loan that offers the best terms

- Use the loan proceeds to pay off all existing debts immediately

- Make one monthly payment on your new consolidation loan

But consolidation isn’t a magic solution. You need decent credit to qualify for attractive rates. If your credit score has taken a hit from late payments, you might not get approved or you’ll face higher interest rates that defeat the purpose.

There’s another risk. Some people consolidate their debts, feel relieved, then start spending on those now-empty credit cards again. Six months later, they’re in worse shape than before.

What debt management plans offer

A debt management plan works differently. You’re not taking out a new loan. Instead, you work with a credit counselling agency that negotiates with your creditors on your behalf.

Credit Counselling Singapore is the main non-profit organization providing this service locally. They contact your creditors to arrange reduced interest rates, waived fees, and extended payment periods.

You make one monthly payment to the counselling agency. They distribute the money to your creditors according to the agreed plan. The process usually takes three to five years to complete.

Here’s what makes debt management plans different:

- Your existing debts stay separate, but payments are coordinated

- Interest rates may be reduced or frozen entirely

- Late fees and penalty charges are often waived

- You receive financial education and budgeting support

- Your credit cards are typically closed during the plan

The biggest advantage? You don’t need good credit to qualify. The counselling agency advocates for you based on your genuine financial hardship.

The downside? Your credit report will show you’re on a debt management plan. This can affect loan applications for several years. Also, not all creditors participate. Some might refuse to negotiate, leaving you to handle those debts separately.

Financial recovery isn’t just about numbers on a spreadsheet. It requires honest self-assessment, consistent discipline, and sometimes the courage to ask for help. Choose the path that addresses not just your debt, but also the habits that created it.

Comparing both approaches side by side

Let’s look at the key differences in a clear format:

| Factor | Debt Consolidation | Debt Management Plan |

|---|---|---|

| Credit score requirement | Good to excellent (typically 650+) | No minimum required |

| How it works | New loan pays off old debts | Agency negotiates with creditors |

| Interest rate impact | Potentially much lower | Reduced or frozen |

| Monthly payment | One payment to lender | One payment to agency |

| Timeline | Depends on loan term (1 to 7 years) | Usually 3 to 5 years |

| Credit report impact | New loan appears, old debts closed | Shows debt management enrollment |

| Access to credit during program | Yes, though not recommended | No, cards typically closed |

| Fees | Interest on loan, possible processing fees | Small monthly fee (around $30 to $50) |

The table makes the trade-offs clear. Consolidation gives you more control and flexibility. Management plans provide structure and support when you’re struggling.

Signs debt consolidation suits your situation

You’re probably a good candidate for debt consolidation if several of these apply:

- Your credit score is above 650

- You can comfortably afford the consolidated monthly payment

- You’re disciplined enough not to rack up new debt

- Your main issue is high interest rates, not inability to pay

- You want to maintain access to credit for emergencies

- You can qualify for an interest rate at least 5% lower than your current average

Many Singaporeans use debt consolidation successfully when they’ve accumulated debt during a specific period (like renovations or wedding expenses) but have stable income to manage repayment.

The strategy works best when you’ve already addressed the spending behaviors that created the debt. If you’re still living beyond your means, consolidation just delays the inevitable.

When debt management makes more sense

Consider a debt management plan if you recognize yourself here:

- You’re missing minimum payments or paying late regularly

- Your credit score has already dropped significantly

- You need help negotiating with aggressive creditors

- You want professional guidance on budgeting and financial planning

- You’re considering bankruptcy but want to try alternatives first

- The total debt feels unmanageable even with lower interest rates

Debt management plans work well for people who need external structure and accountability. The mandatory financial counselling sessions help you understand what went wrong and build better habits.

Many participants appreciate having someone else handle creditor communications. The stress reduction alone can be worth the credit report impact.

Common mistakes that derail both strategies

Regardless of which path you choose, avoid these pitfalls:

- Continuing to use credit cards: This defeats the entire purpose of debt reduction.

- Skipping the budget: You need a realistic spending plan that prevents new debt accumulation.

- Ignoring the root cause: If overspending stems from emotional issues or lifestyle inflation, address those patterns.

- Missing payments: One missed payment can unravel negotiated terms or damage your consolidation loan standing.

- Failing to build emergency savings: Without a buffer, unexpected expenses push you back into debt.

The most successful debt recovery stories share one element. The person didn’t just change their payment structure. They changed their relationship with money.

That’s where building emotional armor becomes relevant. Financial stress affects your mental health. Addressing both together creates lasting change.

The psychological side of debt recovery

Numbers tell only part of the story. Debt creates shame, anxiety, and relationship strain. Many people avoid opening bills or checking their bank balance because the stress feels unbearable.

Choosing between debt consolidation and debt management isn’t purely financial. It’s also about which approach gives you the confidence and support you need right now.

If you’re someone who thrives with independence and self-direction, consolidation might feel empowering. You’re taking charge, making a plan, executing it yourself.

If you’re overwhelmed and need guidance, a debt management plan provides the structure and encouragement that helps you stay on track. There’s no shame in needing support. Recognizing when you need help is actually a sign of strength.

Consider how finding your support network plays into financial recovery. Whether it’s family, friends, or professional counsellors, having people who understand your struggle makes the journey less isolating.

Building financial resilience beyond debt elimination

Paying off debt is the first step. True financial recovery means building systems that prevent future crises.

Start with an emergency fund. Even $50 a month adds up. Building a six-month emergency fund might seem impossible now, but small consistent actions compound over time.

Learn to recognize financial stress early. Understanding when you need to reset helps you address problems before they spiral.

If debt has damaged your credit score, don’t panic. Rebuilding your credit score takes time but follows predictable steps. Each on-time payment moves you closer to recovery.

Making your decision with confidence

Here’s a practical framework for choosing:

Choose debt consolidation if:

– Your credit score qualifies you for rates below 10%

– You have steady income to cover the new payment

– You’re confident you won’t accumulate new debt

– You want to maintain some financial flexibility

Choose debt management if:

– You’re struggling to make minimum payments now

– Your credit score is already impacted

– You need professional support and accountability

– You’re willing to close credit cards during the program

Still unsure? Speak with Credit Counselling Singapore. They offer free consultations and can help you assess which option fits your specific numbers and circumstances.

Don’t let perfect be the enemy of good. Either strategy is better than continuing to struggle with multiple high-interest debts. The best choice is the one you’ll actually follow through on.

Your financial comeback starts with one decision

Facing debt takes courage. Choosing a path forward takes even more. Whether you consolidate or enroll in a management plan, you’re taking control instead of letting circumstances control you.

The road ahead won’t always be smooth. Some months will test your commitment. But thousands of Singaporeans have walked this path before you and emerged stronger on the other side.

Your situation isn’t permanent. Your credit score will recover. Your stress will decrease. Your confidence will return. But only if you take that first step today.

Review your debts tonight. Calculate your monthly obligations. Check your credit score. Then reach out to a bank about consolidation or contact Credit Counselling Singapore about a management plan. Just start. The perfect moment doesn’t exist. This moment is good enough.

Remember, people bounce back not because they never face setbacks, but because they keep moving forward despite them. Your financial comeback story starts now.